MarketTracker East Bay - November 2025 from CharlieBrownSF

The Big Story

Quick Take:

Housing is slowly becoming more affordable, as interest rates slowly creep down over time.

As of the time this is written, the average 30-year mortgage rate is 6.22%, representing a drastic decline from earlier this year.

Inventory levels are holding steady, despite slight increases in transaction volume.

According to the CME FedWatch tool, we’re looking at a 65% chance that the Fed cuts rates by another quarter point in their December meeting.

Note: You can find the charts & graphs for the Big Story at the end of the following section.

*National Association of REALTORS® data is released two months behind, so we estimate the most recent month's data when possible and appropriate.

Housing payments have become slightly more affordable as interest rates tick down

Median monthly P&I payments are on the decline, as one might expect when interest rates are falling. This, of course, is great for new buyers that are in the market for a home. If we see an influx of new buyers, there is the possibility that we might see a less stagnant market when the spring time rush comes in early 2026. Unfortunately though, interest rates are still much too high for many people who locked in rates in the 2-3% range to justify moving to a new home and taking on a considerably higher mortgage payment each month. We likely won’t see these homes/homeowners enter the market until rates come down substantially more than they already have.

The Fed announced yet another quarter point cut to the federal funds rate

In the Fed’s October FOMC meeting, they decided to cut the federal funds rate by another quarter point, making the overnight interest rate range between 3.75% and 4.00%. This led mortgage rates to fall in unison, which is great news for prospective buyers and recent buyers that made the bet that they would be able to refinance at a lower rate sooner rather than later. It’ll be important to look at the economic data that’s released once the government shutdown ends, as this data is what the Fed bases their interest rate decisions on. Once we receive some more clarity regarding economic data, then we’ll have a better idea of whether or not to expect a rate cut in December.

Inventories remain strong despite an increase in transaction volume

Inventories have remained incredibly strong throughout this year, as inventory growth has consistently outstripped existing home sale growth. This past month, we saw inventories grow by 13.97% on a year-over-year basis, while there were only 6.01% more existing homes sold. It’ll be interesting to see where inventories go over the course of the winter, since they usually decline meaningfully.

We may have another rate cut in the not-so-distant future

As we mentioned above, we might have another rate cut ahead of us, as CME’s FedWatch predicts a 65% chance of a 25 basis point rate cut in the Fed’s December meeting. However, it is worth noting that once the government shutdown-related “economic data moratorium” that we’ve been facing is lifted, this probability can shift very rapidly. If economic data is considerably better or worse than anticipated, then this may change how the Fed looks at the cutting cycle that we’re currently in. This means it’ll be very important to keep your eye out for key inflation and labor data once it eventually comes out.

All of this is just what we’re seeing at a national level, though. As we all know, real estate is incredibly localized, which is why you should take a look at your local lowdown below:

Big Story Data

The Local Lowdown

Quick Take:

Median sale prices for condos continue to lag where they were last year.

Inventories are surprisingly static on a year-over-year basis

Listings are spending a lot more time on the market than they were last year.

Note: You can find the charts/graphs for the Local Lowdown at the end of this section.

Little change in single-family home pricing, but condos continue to lag

There was very little change in the single-family home market in the month of October, with the median sale price increasing by 2.00% in Alameda County, and decreasing by 0.81% in Contra Costa County. However, there were some movements in the condo market. This month, the condo market extended its losing streak, as the median condo in Alameda County sold for 9.38% less than it did last year, and the median condo in Contra Costa County sold for 7.69% less than last year. Although these are drastic year-over-year decreases, the market is overall fairly stable, with homes holding their value in the band they’ve created for themselves over the past 8-10 months.

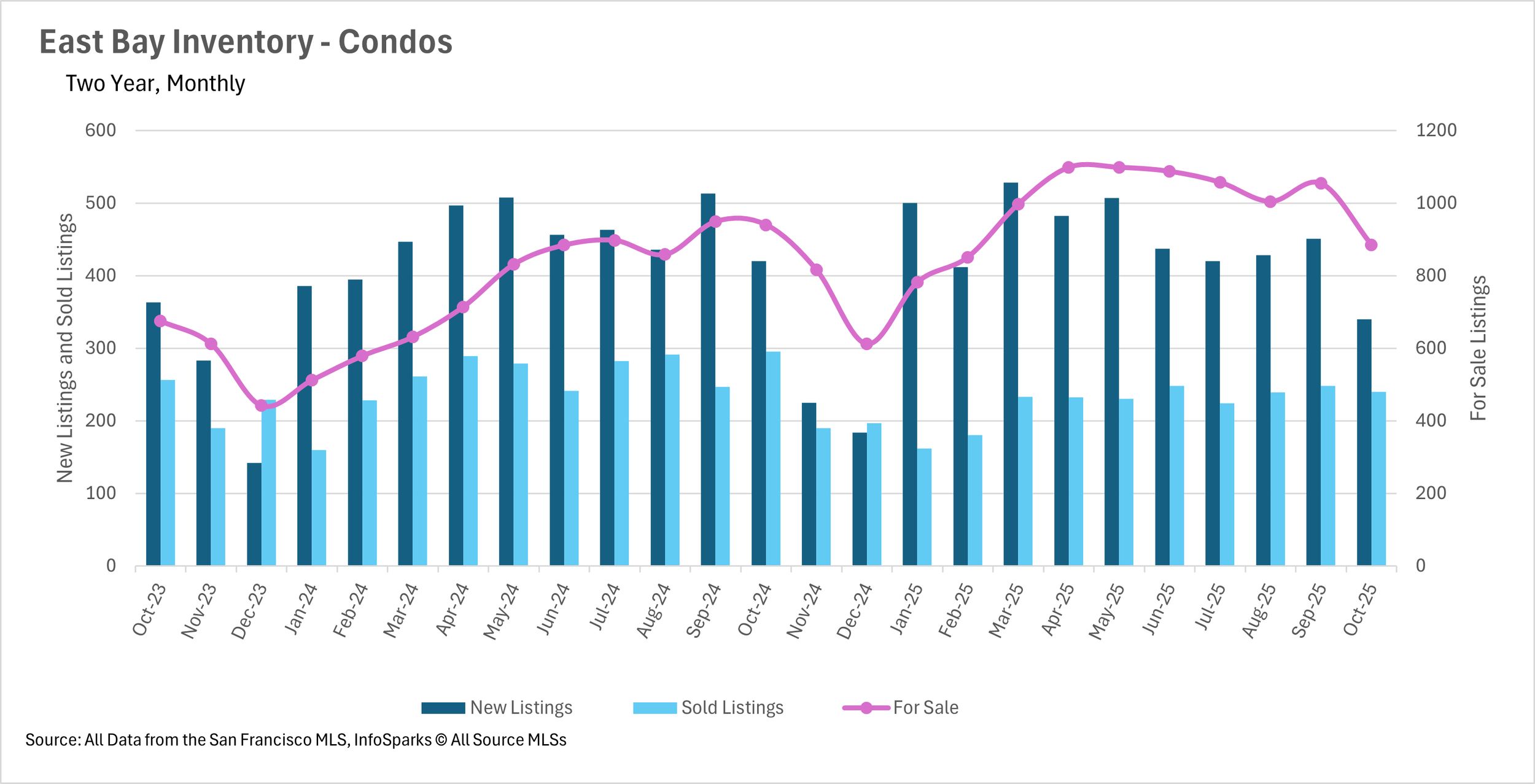

Some interesting developments in condo market inventory levels

Once again, things were more or less business as usual in the single-family home market this month. However, the condo market saw some interesting developments in terms of inventory levels. In the month of October, we saw 19.05% fewer condos listed, and 18.64% fewer condos sold. Active inventory also decreased by 5.85% on a year-over-year basis. It’ll be important to pay attention to how this market evolves over the seasonally slow winter months, as dwindling inventories might drive prices up over time.

Listings are sitting for quite a bit longer than they did last year

In both the single-family and condo markets, listings are sitting on the market for quite a bit longer than they did around this time last year. The average single-family home in Alameda County saw a 7.14% increase in days on market on a year-over-year basis, which seems like a lot. However, these listings still move relatively quickly, with the average listing sold in 15 days. Contra Costa County single-family homes spend an average of 20 days on the market, representing a 33.33% increase year-over-year. When we turn to the condo market, listings are spending many more days on market, with the average listing in Alameda County selling in 30 days (a 50.00% increase year-over-year), and the average listing in Contra Costa County selling in 41 days (a 78.26% increase year-over-year)

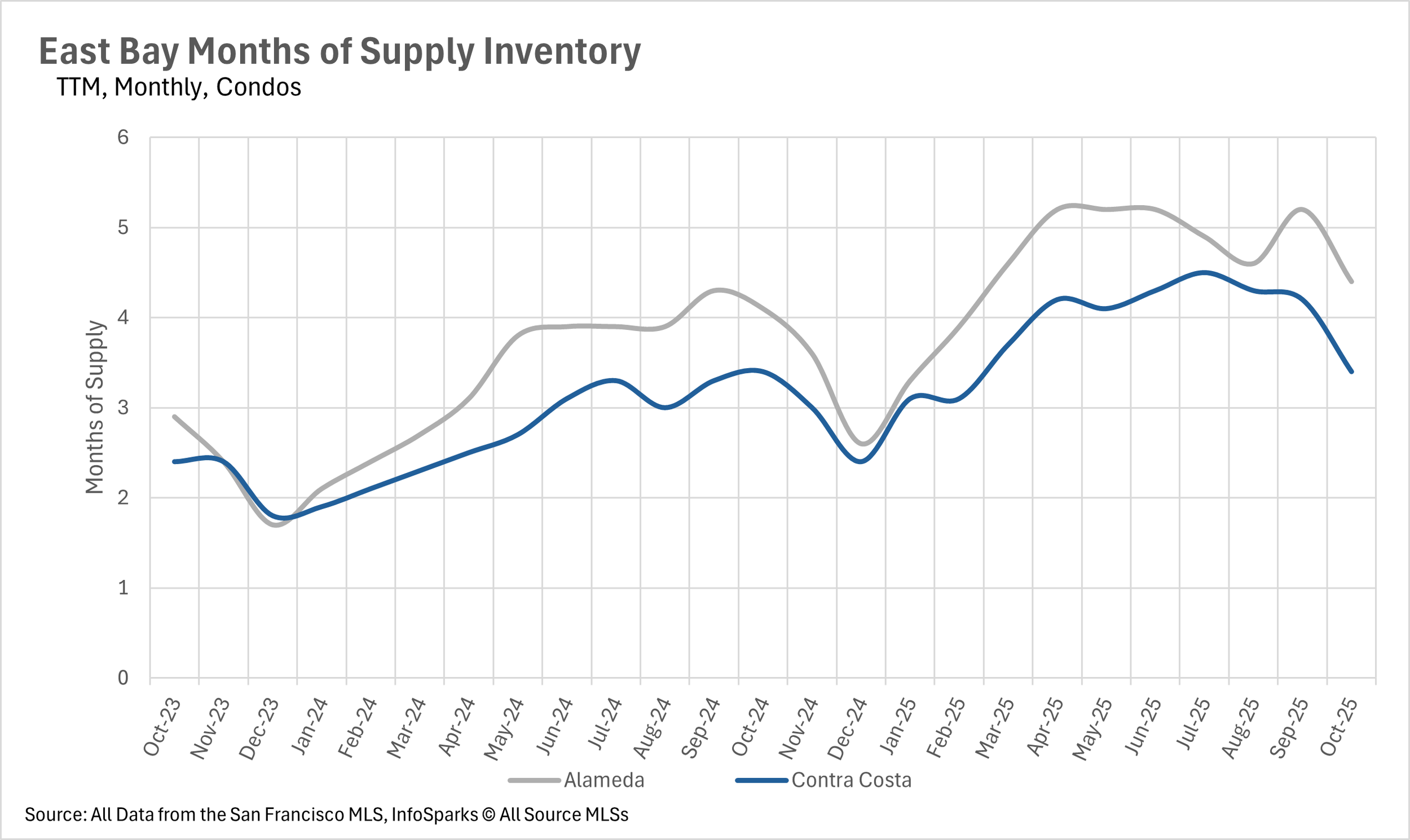

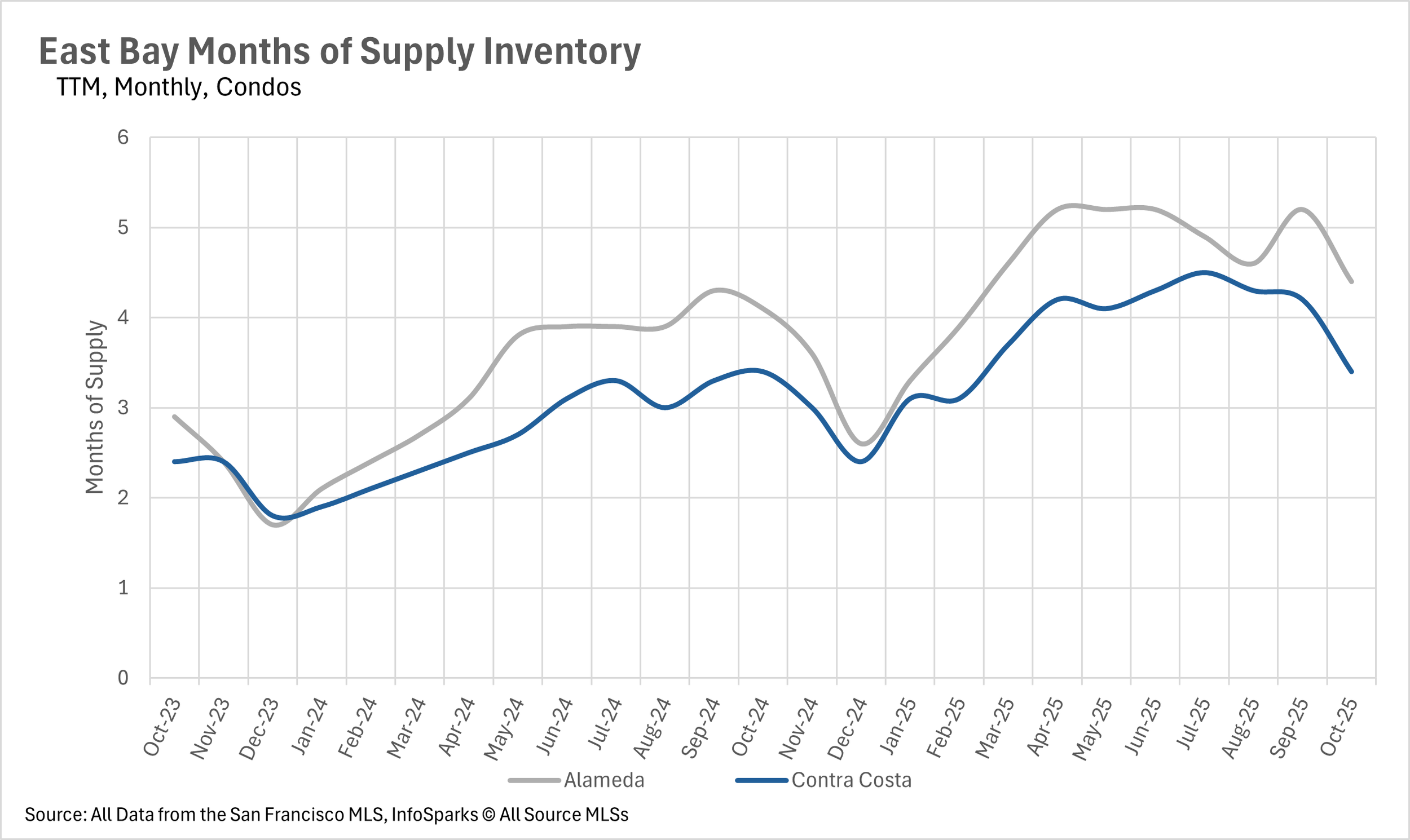

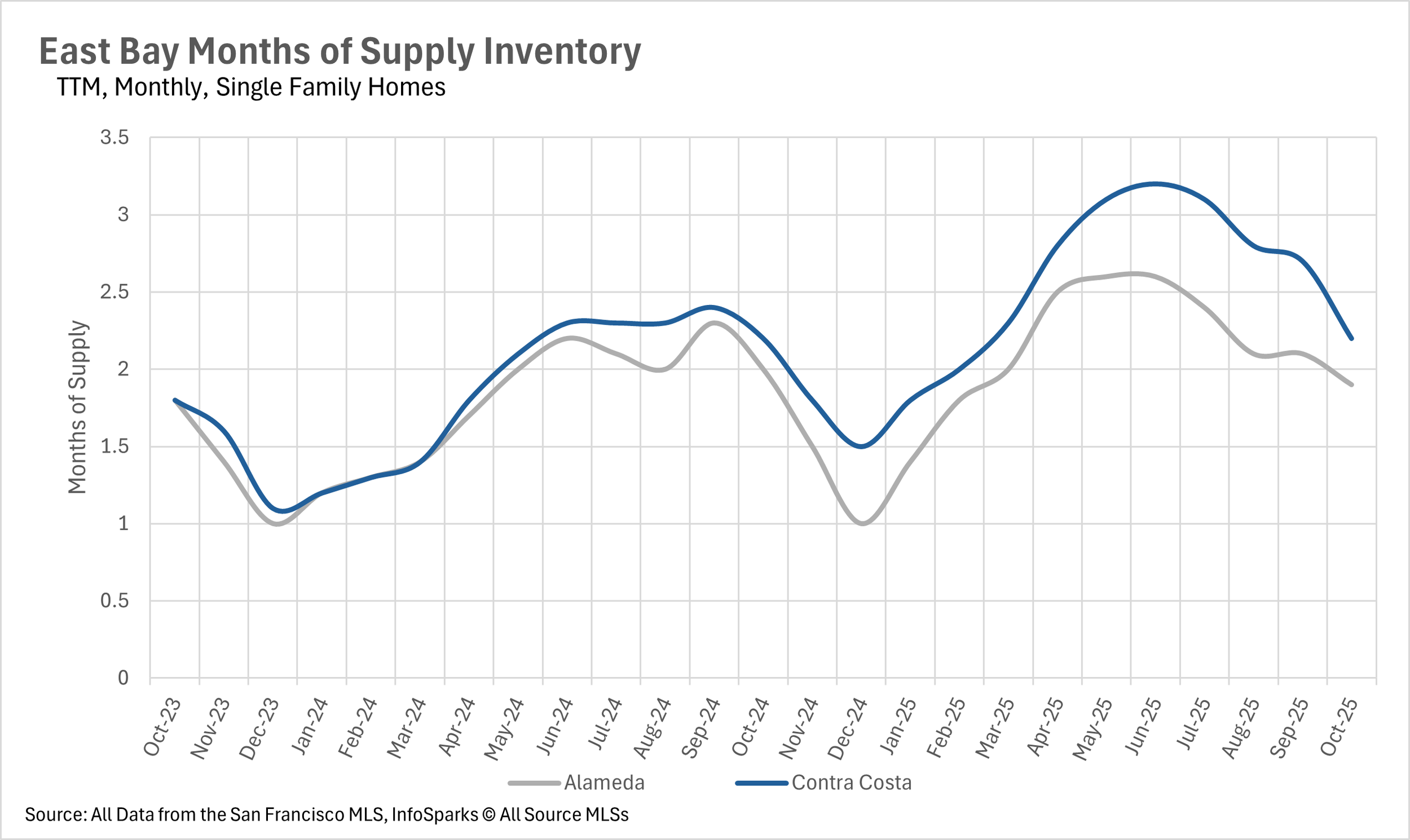

The single-family market is still very competitive, while the condo market is more buyer-friendly

When determining whether a market is a buyers’ market or a sellers’ market, we look to the Months of Supply Inventory (MSI) metric. The state of California has historically averaged around three months of MSI, so any area with at or around three months of MSI is considered a balanced market. Any market that has lower than three months of MSI is considered a seller’s market, whereas markets with more than three months of MSI are considered buyers’ markets.

As per usual, the single-family home market is much more competitive than the condo market. The East Bay is a seller's market when it comes to single-family homes, with Alameda County having 1.9 months of supply on the market, and Contra Costa County having 2.2 months. Whereas the East Bay condo market is a buyer's market, with 4.4 months of supply on the market in Alameda County and 3.4 months of supply on the market in Contra Costa County.